News & Reviews

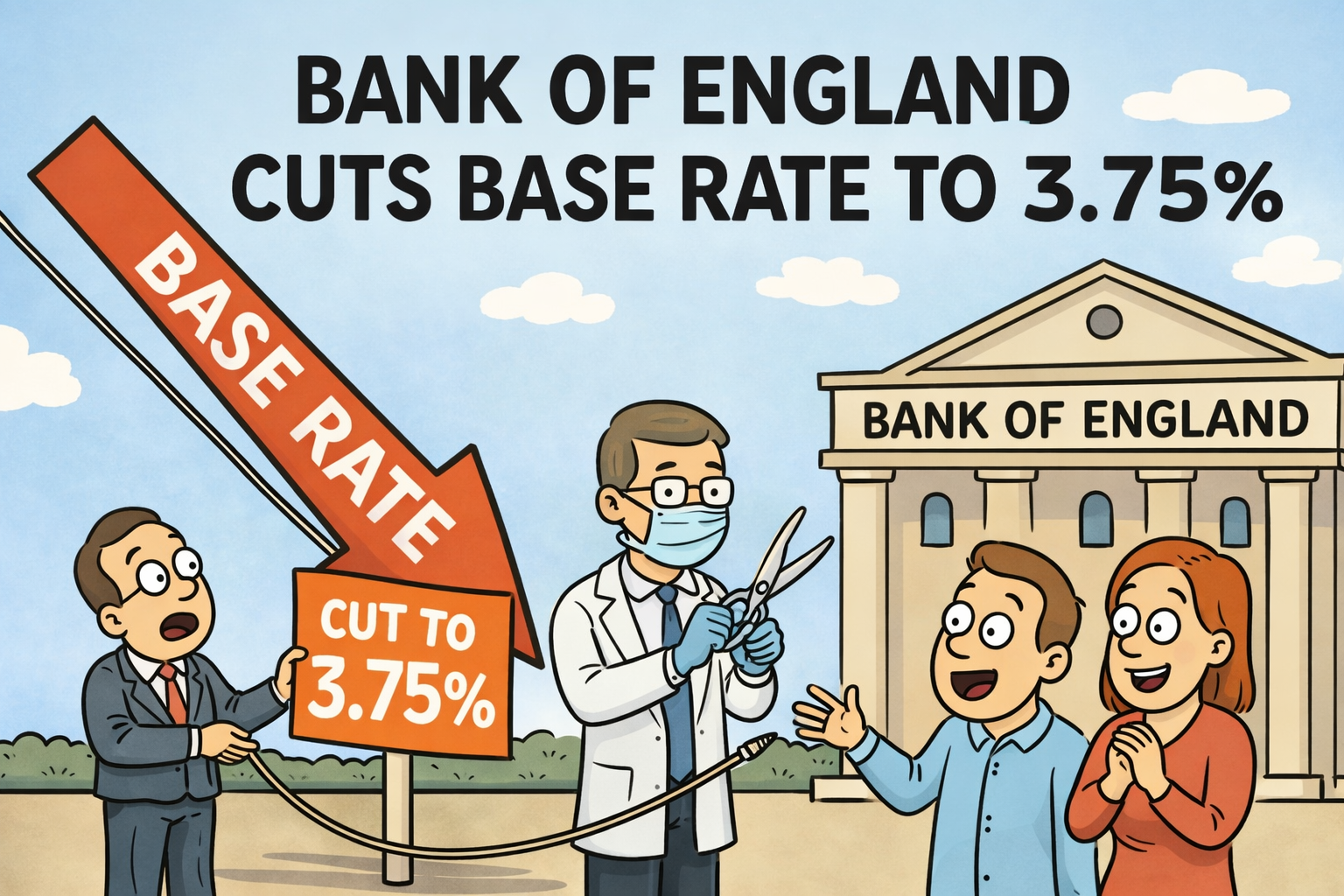

Bank of England Cuts Base Rate to 3.75% - What It Means for Mortgage Borrowers On 18 December 2025 , the Bank of England (BoE) delivered a 0.25% cut to the official base rate , reducing it from 4.00% to 3.75% . This move marks the first reduction since November and aims to provide some support to a slowing UK economy amid easing inflation. What Has Changed? Bank Rate is now 3.75% The Bank’s Monetary Policy Committee (MPC) voted, by a narrow majority, to lower the base rate by a quarter percentage point in response to slowing inflation and softer economic data. This reduction is part of a broader trend of rate cuts seen through 2025 as price growth continues to ease and policymakers look to support growth. What This Means for Mortgage Borrowers Tracker & Variable-Rate Mortgages If you’re on a tracker mortgage or a standard variable rate (SVR) , this cut should feed through into lower monthly repayments- albeit not immediately. Lenders typically adjust their variable products to reflect changes in the base rate, so you may see your monthly payment fall over the coming weeks as lenders update pricing. Fixed-Rate Mortgages For many borrowers on fixed-rate mortgages , your current deal won’t change until it ends. However, new fixed rates are likely to soften , especially on shorter-term products , as competition increases and markets price in the lower Bank Rate. Brokers are already seeing some fixed rates drop nearer to pre-pandemic levels as lenders compete. Remortgagors & Those Coming Off Deals If your fixed deal is expiring soon , this cut could mean more attractive remortgage options - but acting early remains key. It’s worth starting your remortgage search three to six months before your deal ends to capture improving pricing. A lower base rate doesn’t guarantee the lowest deal forever, but markets have responded positively and lenders are reacting. What This Means for the Wider Market Housing Activity Lower borrowing costs can help stimulate housing demand , particularly for first-time buyers and homeowners looking to move or remortgage. Industry commentators are already noting a price-war environment among lenders , which could push two- and five-year fixed rates lower in the weeks ahead . Savers & Other Borrowers If you’re saving money, this cut could see interest rates on savings accounts drift down , as banks and building societies adjust rates across the board. Credit card and unsecured loan rates may also fall, but usually with a lag after base-rate changes. Should You Do Anything Now? Here are a few practical points to consider: ✔️ Review your mortgage deal if it’s nearing expiry - use this cut to compare options now rather than waiting. ✔️ Contact a broker if you’re on a tracker/SVR to understand when your lender updates your rate. ✔️ Don’t delay if you’re planning a purchase - softer pricing could mean better borrowing costs this side of Christmas and into 2026. ✔️ Keep an eye on markets - further base-rate moves aren’t ruled out next year, depending on inflation and economic data. Final Thoughts The BoE’s move to 3.75% is good news for borrowers - particularly those already on variable products or nearing a remortgage. But while cheaper borrowing costs are welcome, the broader economic backdrop remains cautious, and lenders will continue to price risk into mortgage deals . Staying informed and proactive will help you make the most of this easing cycle.

🎉December Prize Draw Winner Announcement🎉 We’re delighted to announce the winner of our Google Review prize draw - congratulations to Dr Adam Richardson, who has won a brand-new pair of AirPods! 🎧 Thank you to everyone who took part and helped make our December draw such a success. We really appreciate the time you take to share your feedback and support us. Missed giving us a review? Don’t panic! If you didn’t get a chance to enter last time, there’s still plenty to play for. We’re running another competition, with the chance to win a pair of AirPods Pro 3. 📅 The next winner will be drawn on 30th April, so there’s still time to get involved. 👉 Click here to leave your review and enter the draw Good luck - and once again, congratulations to Dr Adam Richardson! 🙌

Podcast with Dentists Who Invest – Featuring Sarah Grace | CPD Available In this episode, we discuss how the UK Government’s latest budget changes affect property owners and mortgage holders - especially dentists and small landlords. We explore how shifts in tax bands, interest tax credits, and mortgage pricing are influencing property investment strategies, rental returns, and borrowing decisions. We also share practical tips on approaching fixed-rate mortgage deals and preparing the right documentation, whether you’re remortgaging, buying a home, or considering buy-to-let. 📌 Key takeaways: 📉 Interest rates: Fixed rates (2 and 5-year deals) are easing as markets digest the budget, but uncertainty remains. 💸 Tax impact: Changes in tax bands and interest tax credits can pull more rental income into higher rates. 🔑 Strategy tip: If your current mortgage fix is ending soon, consider securing a product now to cap risk and switch later if prices fall. 🧠 Practical guidance: Covers what documents to gather and how to choose between mortgage terms. 📍 For higher-value homes: Be aware of proposed mansion tax bands and valuation timing ahead of 2028. ➡️ Great listen if you’re navigating property finance in the current UK market! 🎧 Listen now : The Budget And Your Properties/Mortgage 📝 CPD Certificate Available : This episode is eligible for verified CPD, making it a valuable use of your time both personally and professionally.

What our customers say

Great as always. Having used Sarah’s services on a few occasions now, I have had great support and brilliant communication in order to get the best end result. I have recommended her to several friends, family and business associates. I look forward to working closely with Sarah and her team in the future.

Dr G Singh – Associate Dentist

Just to say a huge Thank you to both Sarah and Jordan for a superb service throughout a tortuous process. Your kindness and good humour helped to keep us sane and we appreciated that you continued to take an interest in us right until the day we completed. I couldn’t recommend you highly enough!!

Ms A Alison

A very much more relaxing and less time consuming experience than trying to deal with any of the banks I had tried. I would recommend at least speaking with Sarah Grace Mortgages if you need a mortgage. It is very likely they can help you.

Mr C Millard

My slightly unusual circumstances didn’t lend themselves to the factory approach that I encountered when I talked directly to various mortgage providers. I would not hesitate to recommend Sarah Grace to anyone looking for a mortgage.

Andy Follows – Managing Director of Aquilae

The service I received from Sarah and Jordan has been fantastic. I was kept fully informed throughout the whole application process. Sarah and her team took care of everything and liaised with all relevant parties on my behalf making the whole process hassle free. I would highly recommend them to all family and friends.